Trump Accounts: The Ultimate Tax-Free Wealth Strategy for Kids

Trump Accounts can be an excellent jump start to a child or grandchild's retirement savings.

Is the Trump Account the most powerful tax-free wealth strategy for the next generation? Irrespective of your political leanings, you need to know about this new financial tool. Officially created under the 'One Big Beautiful Bill,' these are formally known as Section 530A accounts.

Think of them as a "Starter IRA" for kids. When executed properly, they act effectively as a custodial Roth IRA, providing a massive head start for investing for children or grandchildren.

Trump Account Eligibility and Contribution Limits

Who is eligible? Any child under the age of 18 with a Social Security Number can have an account.

The Deadline: The account must be opened before the end of the calendar year the child turns 18.

Annual Limit: Individual contributions from parents, grandparents, and relatives are capped at a combined $5,000 per year.

No Income Required: Unlike a standard Roth or Traditional IRA, the child does not need to have earned income for you to contribute.

The $1,000 Kickstart: If your child was born between January 1, 2025, and December 31, 2028, the government seeds the account with a one-time $1,000 deposit.

The Employer Match Perk

There is a massive perk for employees under Section 128. Your employer can contribute up to $2,500 of that $5,000 annual limit tax-free to you. This match does not count as taxable income, essentially providing "free money" to build your child's wealth.

The "Secret Sauce": Converting a Trump Account to a Roth IRA

The real power of the Trump Account lies in IRS Notice 2025-68. When the child turns 18, the account legally converts into the framework of a Traditional IRA. This makes it eligible for Roth Conversions.

By making partial Roth conversions over 3–4 years while the child is in college (and likely has low or zero income), you can leverage the standard deduction. This strategy allows you to move the entire balance into a Roth IRA without paying a single cent in federal income tax.

Trump Account Investment Restrictions & Tax Treatment

During the "Growth Period" (before the child turns 18), you are restricted to "Eligible Investments."

What to buy: Low-cost, passive mutual funds or ETFs tracking broad US indices.

The Cost: The expense ratio must be under 0.10%.

Tax Treatment: Contributions are made with after-tax dollars (no federal deduction). Growth is tax-deferred, meaning no annual taxes on dividends or capital gains.

Note on State Taxes: While tax-deferred federally, states like California, Massachusetts, and Pennsylvania may treat annual earnings as taxable income. Always check your specific state's "kiddie tax" guidance.

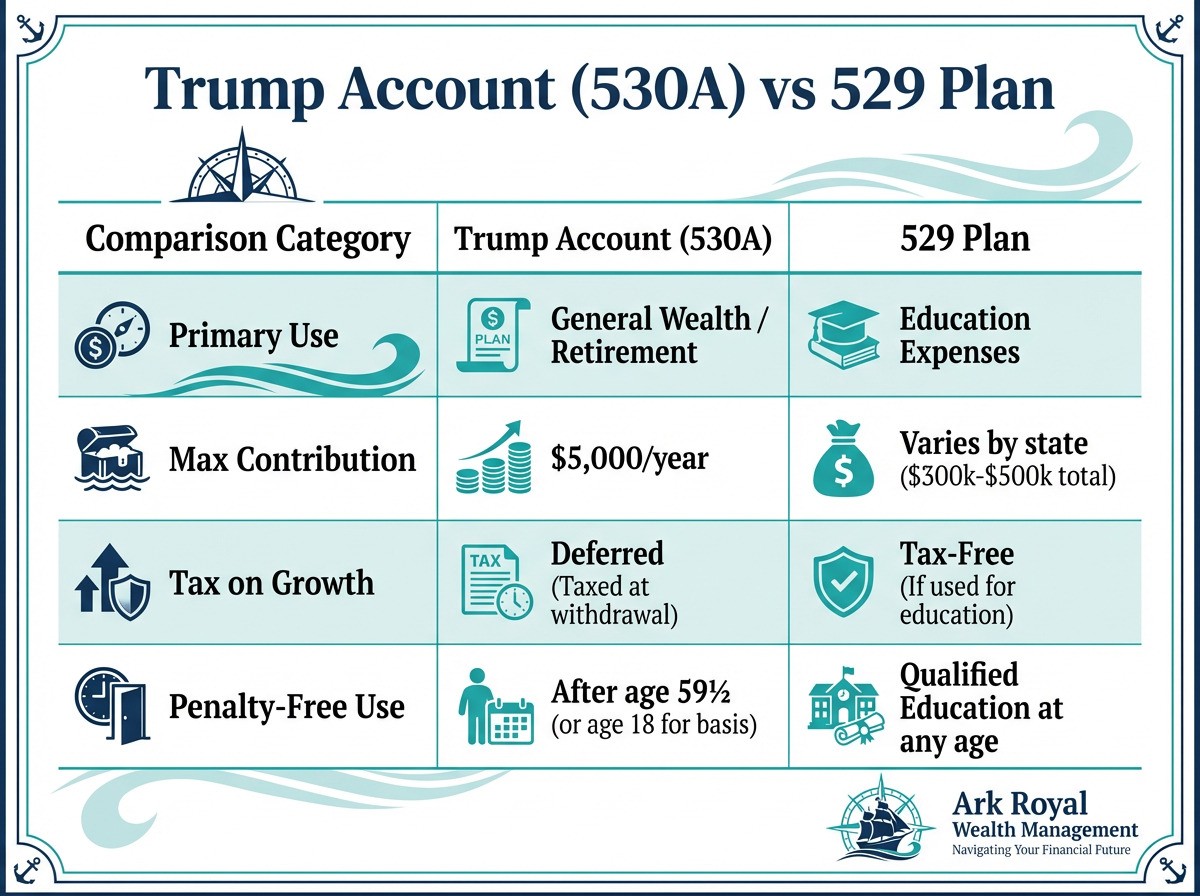

Comparing Trump Accounts to 529 Plans

Some of our clients have asked whether they should contribute to Trump Accounts or 529s for their grandchildren. The chart below outlines key differences between Trump Accounts and 529 accounts.