Understanding Index Funds: Reconstitution and Tracking Error

Investors in index funds may sacrifice return and diversification at the expense of tracking errorIndex funds have gained immense popularity as an investment strategy, offering a low-cost and diversified means for investors to mirror the performance of a market index.

Investors in index funds may sacrifice return and diversification at the expense of tracking error

Index funds have gained immense popularity as an investment strategy, offering a low-cost and diversified means for investors to mirror the performance of a market index. However, a critical aspect of index fund management is ensuring that the fund remains aligned with its benchmark index. This involves achieving zero tracking error and regularly reconstituting the fund's holdings in accordance with the relevant index.

What is Tracking Error and Why is It Important?

Tracking error measures the difference between the performance of an index fund or ETF versus its benchmark index. It quantifies how closely the portfolio's returns match those of the index it aims to replicate. A smaller tracking error indicates that the portfolio's performance closely follows the benchmark, while a larger tracking error suggests a significant deviation.

Index funds (whether they are mutual funds or ETFs) aim for zero or low tracking error. Achieving zero tracking error is challenging and requires meticulous management, especially during the reconstitution process.

What is Index Reconstitution?

Reconstitution is the periodic process of updating the components of an index to reflect changes in the market. These changes can result from various factors, such as shifts in company size, mergers, or changes in a company's financial health. The primary goal of reconstitution is to maintain the accuracy and relevance of the index, ensuring it continues to represent the market segment it was designed to track.

During reconstitution, fund managers must adjust the holdings within the index fund to match the updated composition of the benchmark index.

This process might involve:

Adding new companies that now meet the index's criteria.

Removing companies that no longer qualify for inclusion.

The criteria for these adjustments are set by the organizations that develop the indices (Standard & Poors for the S&P 500 index for example) and they are applied rigorously. The frequency of reconstitution varies, typically occurring quarterly, semi-annually, or annually. This regular updating process is essential for keeping the index fund in line with its benchmark, but it can also lead to significant changes in the fund's composition. Index providers announce the changes and the effective date well in advance of the effective change.

The Impact of Reconstitution

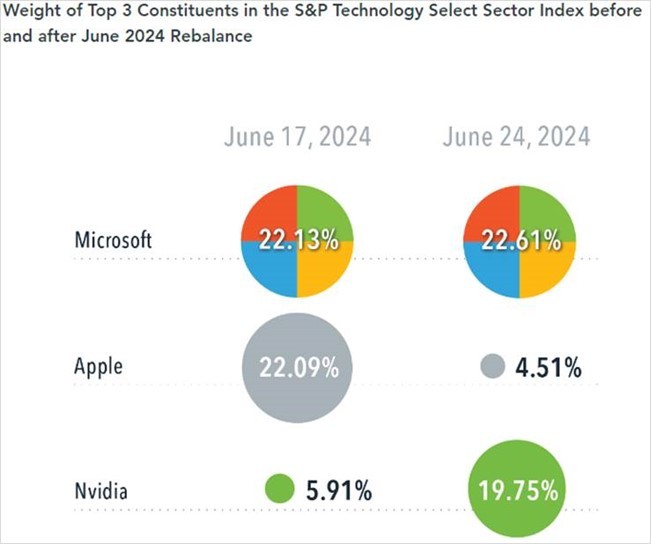

Reconstitution can sometimes result in dramatic shifts in a fund's holdings. For instance, during a reconstitution event, the allocation to a specific sector or stock might significantly increase or decrease based on the index's new criteria. Such changes can sometimes surprise investors, who may not realize the extent of these adjustments.For example, during a recent reconstitution of the S&P Technology Select Sector Index, the allocation to Apple decreased by 17.5%, while Nvidia's weight increased by 13.8%.

Such large shifts highlight the potential drawbacks of strictly adhering to index rules, as they can lead to substantial changes in a fund's exposure to certain stocks or sectors. Investors may not always be aware of these changes, yet they can significantly impact the fund's performance and risk profile. Ironically, this index has close to 50% in just 3 stocks! That hardly seems like appropriate diversification.

Why Dimensional Fund Advisors (DFA) Offers a Better Investment Solution

While index funds offer a straightforward and cost-effective way to invest, it's crucial for investors to understand the mechanics behind them, particularly the process of reconstitution. We think a better approach is an investment strategy that relies on sound academic research (like index funds) but has the benefit of flexibility - that's the approach Dimensional takes. We think being compelled to buy or sell based on some arbitrary dogmatic adherence to rules is likely to work against the investor.