What the NC Department of Insurance Discovered at Capital Financial & Insurance and What Clients of Capital Financial Advisory Group Should Know

We recently uncovered unsettling information about Capital Financial & Insurance (CF&I), a business affiliated with Capital Financial Advisory Group (CFAG). CF&I administers insurance product sales to clients of CFAG. Both CFAG & CF&I are majority owned by "Coach" Pete D'Arruda.

We recently uncovered unsettling information about Capital Financial & Insurance (CF&I), a business affiliated with Capital Financial Advisory Group (CFAG). CF&I administers insurance product sales to clients of CFAG. Both CFAG & CF&I are majority owned by "Coach" Pete D'Arruda.

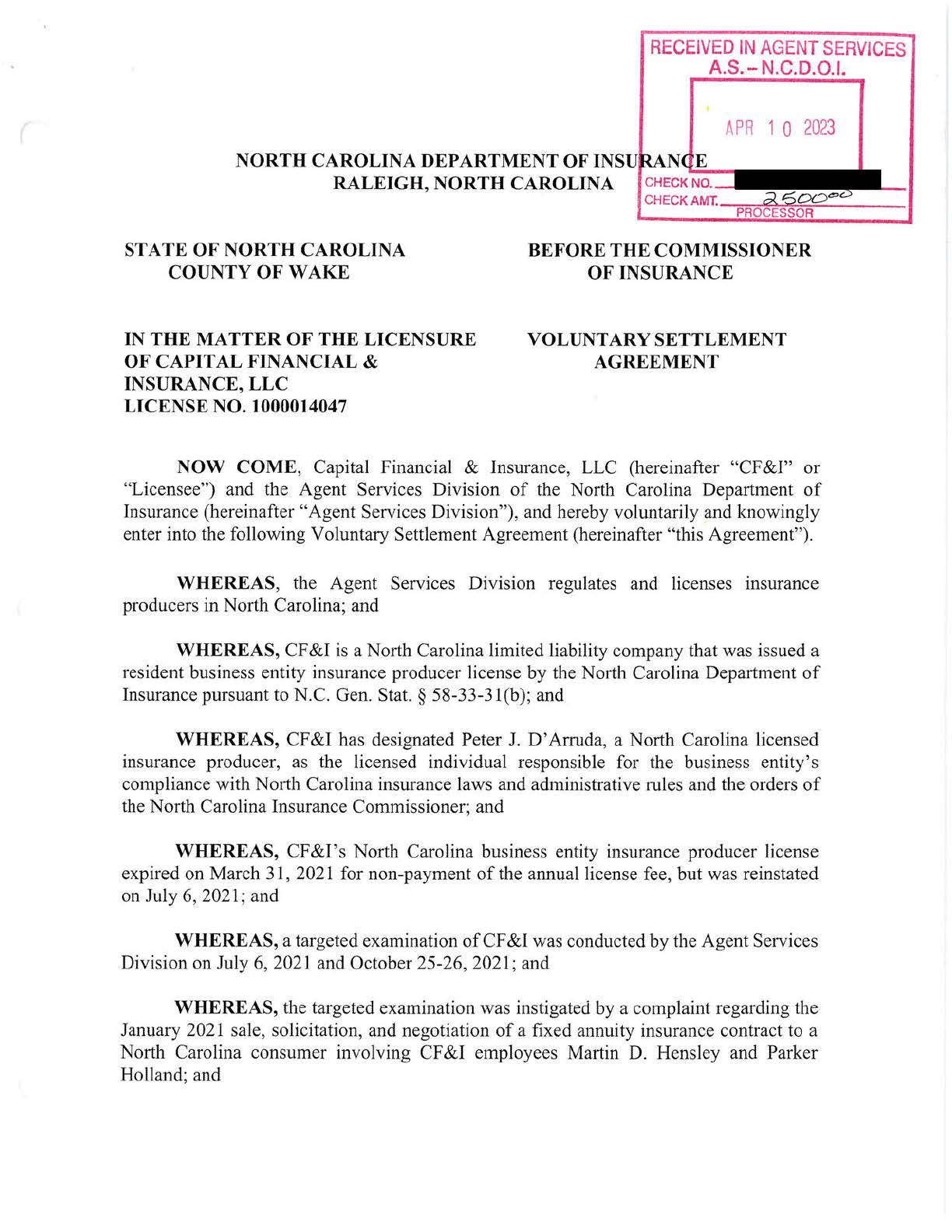

Public records show that the NC Department of Insurance (NCDOI), the state agency that enforces insurance sales regulations, found CF&I violated several North Carolina General Statutes (NCGS). The NCDOI conducted a targeted exam as the result of a consumer complaint related to an annuity sale involving Marty Hensley and Parker Holland, advisors with CFAG. As a result of their investigation, the NCDOI entered into a Voluntary Settlement Agreement with CF&I and fined them $2,500. As an editorial aside, $2,500 hardly seems like a punitive fine, especially given the lucrative fees associated with fixed index annuity sales. It makes one question whether regulators are truly committed to protecting consumers.

You can find the settlement agreement here: https://www.ncdoi.gov/capital-financial-insurance-llc-1000014047/open

What NCDOI Found Wrong at Capital Financial

The NCDOI investigation found that Marty Hensley presented clients with financial plans, outlined benefits, terms and conditions of insurance products and received commissions and fees for the sale of insurance products despite not having an insurance license for 49 months. They also found that CF&I's insurance producer license expired for 3 months for non-payment of the annual license fee.

North Carolina Law and the Penalty for Unlicensed Insurance Sales

In North Carolina, the sale of an insurance product (including a fixed index annuity), requires a specific insurance license. Selling an insurance product without the appropriate license is a violation of the NC General Statutes.

NCGS § 58-33-82(b) strictly forbids any person from accepting a commission, service fee, or other valuable consideration for selling, soliciting, or negotiating insurance in North Carolina if they are required to be licensed and are not so licensed.

NCGS § 58-33-82(a) prohibits insurance companies or licensed producers from paying a commission to an unlicensed person for selling insurance.

The Remedies for Violations

If advisors or insurance brokers are found in violation of insurance laws the remedy for violating such laws falls under the administrative authority of the North Carolina Department of Insurance (NCDOI). There are several remedies available:

The Insurance Commissioner may order the advisor or business entity to pay a civil penalty (fine).

The NCDOI has the power to revoke or suspend the insurance producer's license.

The Insurance Commissioner can petition the Superior Court to order payment of restitution to the affected consumers.

What Should You Do If You Believe You Were Misled by CFAG?

Depending on when you bought your annuity and who was involved in the sale – you may be able to seek one of the remedies outlined above, including either repayment of surrender fees or the rescission of your annuity contract. We’ve helped a number of former CFAG clients get favorable outcomes, give us a call if you’d like to learn more about your options.

Fixed Index Annuities are Complicated Products – Proceed with Caution

Many brokers selling fixed index annuities make them seem simple – claiming they capture the upside of the stock market with no downside, the reality is buried in the fine print. See our YouTube video on fixed index annuities here: Fixed Index Annuities Explained: What You Need to Know Before Investing

These products are very complicated and here are just some of the things you need to understand before purchasing a fixed index annuity:

Caps and Participation Rates: Your contract's earnings are typically limited by features like an annual interest cap or a participation rate. For instance, if the index rises 12% but your contract has a 7% cap, your gain for the year is limited to 7%. Higher participation rates come with additional fees.

Lack of Flexibility: FIAs are highly illiquid, limiting the amount you can withdraw without steep fees.

Unfavorable Tax Treatment: Any income you do receive is taxed at higher ordinary income tax rates.

Conflict of Interest: FIAs can be sold based on conflicted advice, prioritizing the advisor's commission (which can be substantial) over the client's financial interests.

High Fees That Can Be Hard to Uncover: FIAs are often riddled with murky and hard to decipher fees and charges. And finding them within the contract or marketing material can challenge even sophisticated investors.

During the most critical financial phase of life you need to know you're working with an advisory firm you can trust, one that plays by the rules, doesn't shortcut the process and always puts your interest first. If you are seeking that type of relationship, let's talk.